The Microelectronics Chessboard: Initial Moves Towards Resilience:

Unveiling the US-China Microelectronics and Rare Earth's Dilemma, and the Journey Beyond the CHIPS Act

Currently, China has the most untapped deposits of rare earth minerals. But, in the heart of Africa lies a treasure often overlooked, a mine rich with rare earth elements, the lifeblood of modern technology. As dawn breaks, the miners at a mine backed by a U.S. joint venture funded through DFC brace themselves for a day of toil under the sun, extracting minerals destined to power gadgets across the globe. The extracted ores embark on a journey that epitomizes the global microelectronics supply chain and many other sectors, weaving through continents, shaping economies, and underlining the strategic tussle between superpowers.

The bounty from the African mine soon finds its way to a sophisticated smelting and refining facility in China, the global epicenter of rare earth processing. Amidst a maze of pipelines and furnaces, the raw ores are meticulously refined, transforming into valuable materials ready to fuel the microelectronics sector. Lynas Corporation, another titan in the rare earth industry, sends its yield from its mines to its new processing facility in Malaysia in hopes of changing reliance on Chinese refining, underscoring the global nature of this supply chain.

As 97% of the world’s refined materials exit the Chinese facility, they carry proof of the Chinese dominance in the microelectronics realm. They are shipped to manufacturing behemoths like Taiwan Semiconductor Manufacturing Co Ltd (TSMC), where they play a pivotal role in churning out semiconductors that form the heart of modern electronic devices. TSMC, with its state-of-the-art facilities, epitomizes the precision and innovation required in semiconductor manufacturing and other sectors outside of semis like E.V. batteries.

Across the Pacific, anticipation builds as the shipment docks on American shores. The precious cargo is delivered to tech giants like Nvidia, where it fuels the creation of cutting-edge computing solutions. As Nvidia unveils its latest microchip, the journey of the rare earth elements reaches fruition. They now reside in the gadgets that power the lives of millions of Americans, a silent testimony to a global supply chain that begins in the heart of Africa or Latin America and eventually arrives in China before moving to companies in South Korea, Taiwan, and the U.S.

Yet, beneath this tale of global commerce lies a stark reminder of strategic competition. The microelectronics, E.V. Batteries, and other supply chains, exemplified by the odyssey of rare earth elements, are a theater where the U.S. and China vie for dominance. The actions of M.P. Materials, Lynas, TSMC, and Nvidia are not mere commercial endeavors; they are moves in a grander geopolitical chessboard, each striving to secure a favorable position in a landscape where control over microelectronics equates to power, influence, and security.

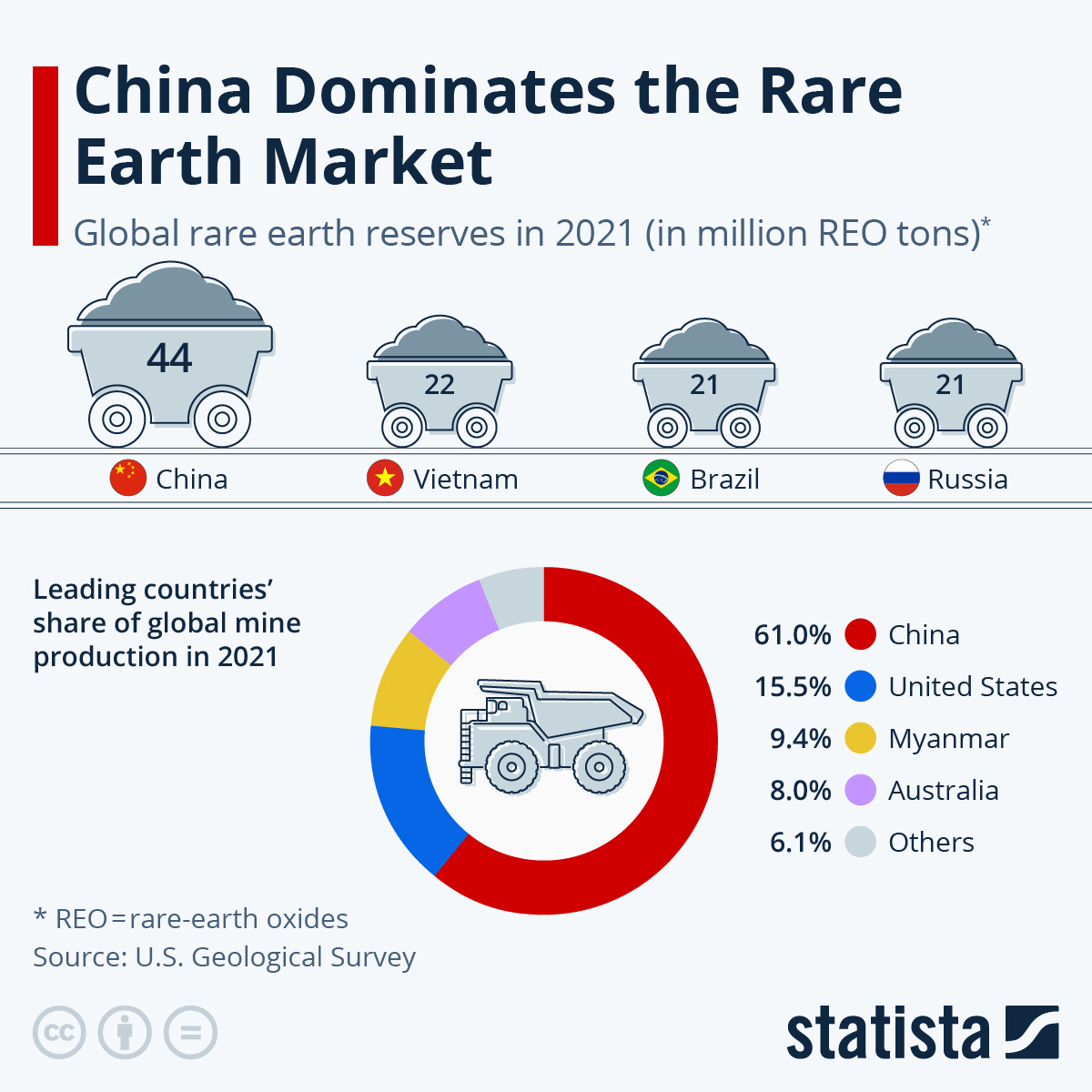

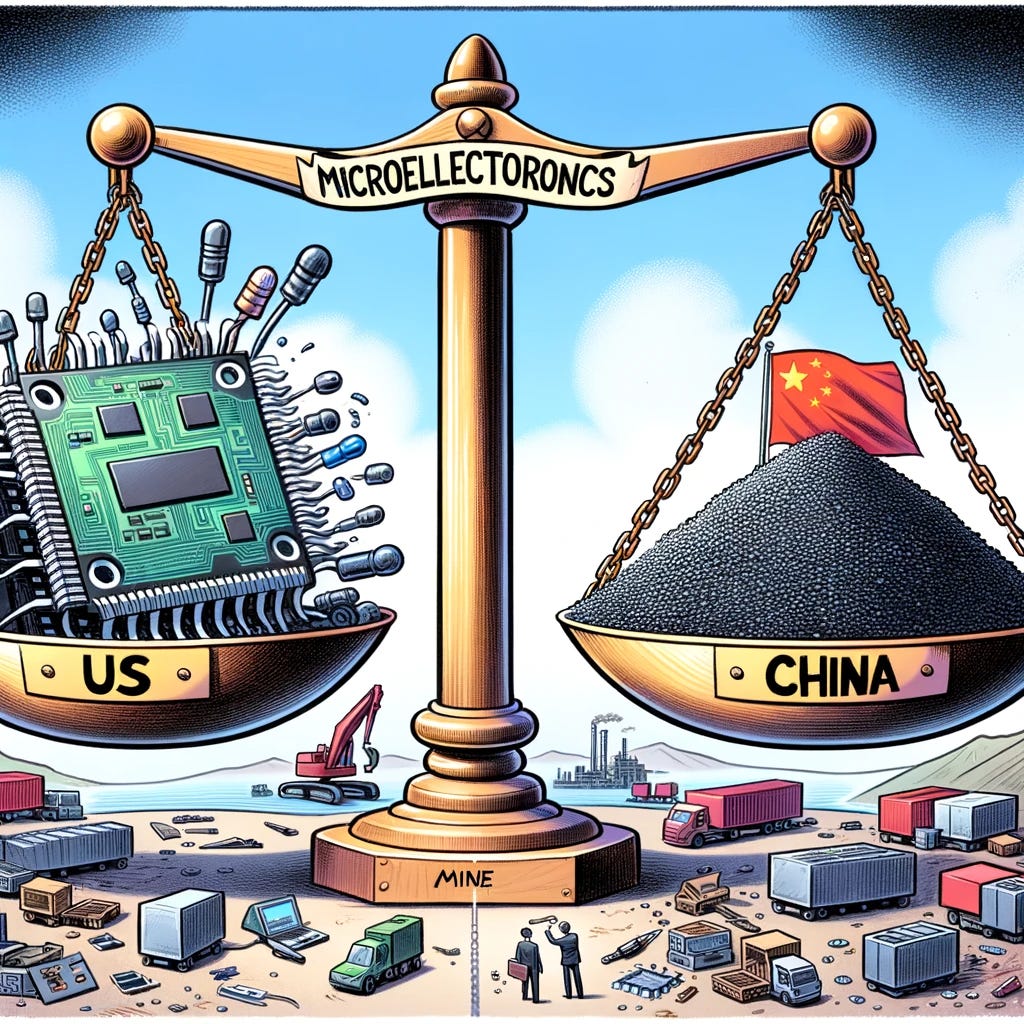

The global microelectronics sector is emblematic of the modern age, underpinning myriad technologies that fuel the 21st-century economy. At the heart of this sector lies the intricate process from the smelting and refining of rare earth elements to the final production of microelectronic devices. Dominance in this sector has been decisively seized by China, a reality that carries profound macroeconomic implications worldwide, especially for the United States.

The journey of rare earth elements, indispensable for microelectronics, commences in mines and culminates in sophisticated gadgets. China’s command over this supply chain is nearly absolute, courtesy of its vast rare earth reserves and robust industrial infrastructure and the ability to subsidize Chinese companies who undercut prices to operate at a loss to secure dependence on China by its new “business partners.” The smelting and refining of rare earths, a critical yet under-emphasized phase, is where China has significantly outpaced other nations. This control enables China to monopolize the production of essential components like semiconductors virtually, establishing a stranglehold on the global microelectronics arena.

The economic repercussions of this dominance are far-reaching. By monopolizing a sector intrinsic to modern technologies, China has positioned itself as an indispensable supplier to global markets. The ripple effects of this concentration of production and supply are felt globally, with economies becoming inadvertently tethered to China’s industrial apparatus. This reality renders international markets susceptible to any disruptions or policy shifts emanating from Beijing.

The recent export restrictions on graphite and other rare earth elements by the Chinese Communist Party are harbingers of a precarious dependency. The United States, a significant consumer of microelectronic products, finds itself in a particularly vulnerable position. A cessation or even a reduction in supply from China could precipitate a crisis in the microelectronics sector, hampering technological advancement and inflating prices. Such a scenario would not only impede economic growth but also erode the purchasing power of American consumers.

The burgeoning competition between the U.S. and China is often framed within a broader geopolitical narrative. However, the microelectronics sector is where this rivalry is most palpable. The U.S., with its technological prowess, has the potential to challenge China’s dominance. Yet, the lack of a domestic supply chain, from the mining of rare earths to finished microelectronics production, is a glaring Achilles’ heel. The current supply chain model, heavily reliant on China, is untenable if the U.S. aims to vie for supremacy in this critical sector.

The U.S. must orchestrate a strategic redeployment of the microelectrU.S.ics supply chain. Diversifying the sources of rare earth elements and fostering domestic production capacities are crucial steps toward mitigating the risks associated with over-reliance on a single nation. Moreover, galvanizing alliances with other technologically advanced countries could engender a more balanced global microelectronics ecosystem.

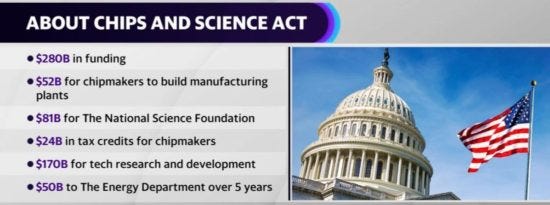

The urgency for action is palpable. The U.S. has taken a significant step through the CHIPS and Science Act, investing in a robust, self-sustaining microelectronics sector to meet domestic demands and compete globally, which also serves as a bulwark against supply disruptions and a move towards technological self-reliance and economic resilience. However, while the Act provides a solid foundation, it fails to address the expedited refining of rare earth materials, a crucial component for semiconductor manufacturing. This gap may hinder the speed at which the U.S. attains complete self-sufficiency and global competitiveness in the microelectronics domain.

There are still ways to capitalize on this type of market uncertainty. Investing in companies like Lynas Corporation or M.P. Materials, which are at the forefront of diversifying the rare earth processing supply chain outside China, holds potential. Also, backing firms like TSMC and Nvidia, critical players in semiconductor manufacturing, or even supporting new smelting and refining facilities outside China can be viable options. Lastly, monitoring the implementation of legislative measures like the CHIPS Act and aligning investments towards companies poised to benefit from such policies could yield long-term gains.

The road ahead is laden with challenges, yet the stakes are too high for complacency. As the microelectronics sector continues to burgeon, the imperative for a strategic re-evaluation and reconfiguration of the existing supply chain paradigms cannot be overstated. The tussle for dominance in the microelectronics sector is not merely an economic contest; it is a pivotal frontier in the broader US-China strategic competition. In this high-stakes contest, redefining the microelectronics supply chain is not just a competitive advantage; it is a national imperative.

You have truly stepped up you graphics game.

Do you outsource your graphics?