The Fools Golden Era

Britain is broke, stagnant, and about to hand the keys to a man who treats the bond market as a minor inconvenience. We've seen this film. We know the ending.

There’s a particular sound a middle power makes on the way down. It isn’t a bang. It’s the quiet shuffle of a trade delegation boarding a plane to Beijing, hats in hand, hoping the people there tell them warm things and make promises they have no intentions to keep but that sound great to their domestic audience.

In late January, Keir Starmer became the first British prime minister to set foot in China in eight years. He brought sixty businesses with him. Bank chairmen, the bosses of the country’s best drugmakers, a delegation assembled with the particular urgency of a man who has run clean out of other ideas. He flew home with £2.2 billion in “export deals” and a tariff cut on Scotch whisky, from 10% down to 5%. The British press called it a reset.

We have a different word for it. We call it tribute.

A scholar at Oxford’s China Centre said it better than we could. The bet Britain placed on China back in the Osborne years, he argued, had “categorically” not paid off. It had “opened the doors wide to dependency... And all for what? Very little in terms of trade and economic benefit for the UK. I’d call this period – for the UK at least – the ‘fool’s golden era.’”

The fool’s golden era. We’re stealing the phrase, and we’re going to walk you through, line by line, why the sequel is going to be worse than the original. And why the man most likely to be running Britain by autumn is the last person you’d want at the wheel when the road finally runs out.

Get a coffee. This one bites.

Part I: The patient is not “fine”

Start with the official story, because the official story is a small masterpiece of denial.

The number-crunchers will tell you Britain is muddling through. They’ll wave at a first-quarter growth print of 0.6%, fastest in the G7 that quarter, and exhale. They’ll note that British sovereign credit-default swaps trade somewhere around 15 to 17 basis points, which is the market’s way of saying the odds of Britain actually defaulting round to zero. No crisis here. Move along, nothing to see.

We’d like to introduce these people to the concept of kindling.

A house that hasn’t caught fire yet is not the same thing as a house that won’t. Look past the flattering quarter, into the actual timbers of the British economy, and what you find is bone dry and stacked to the rafters.

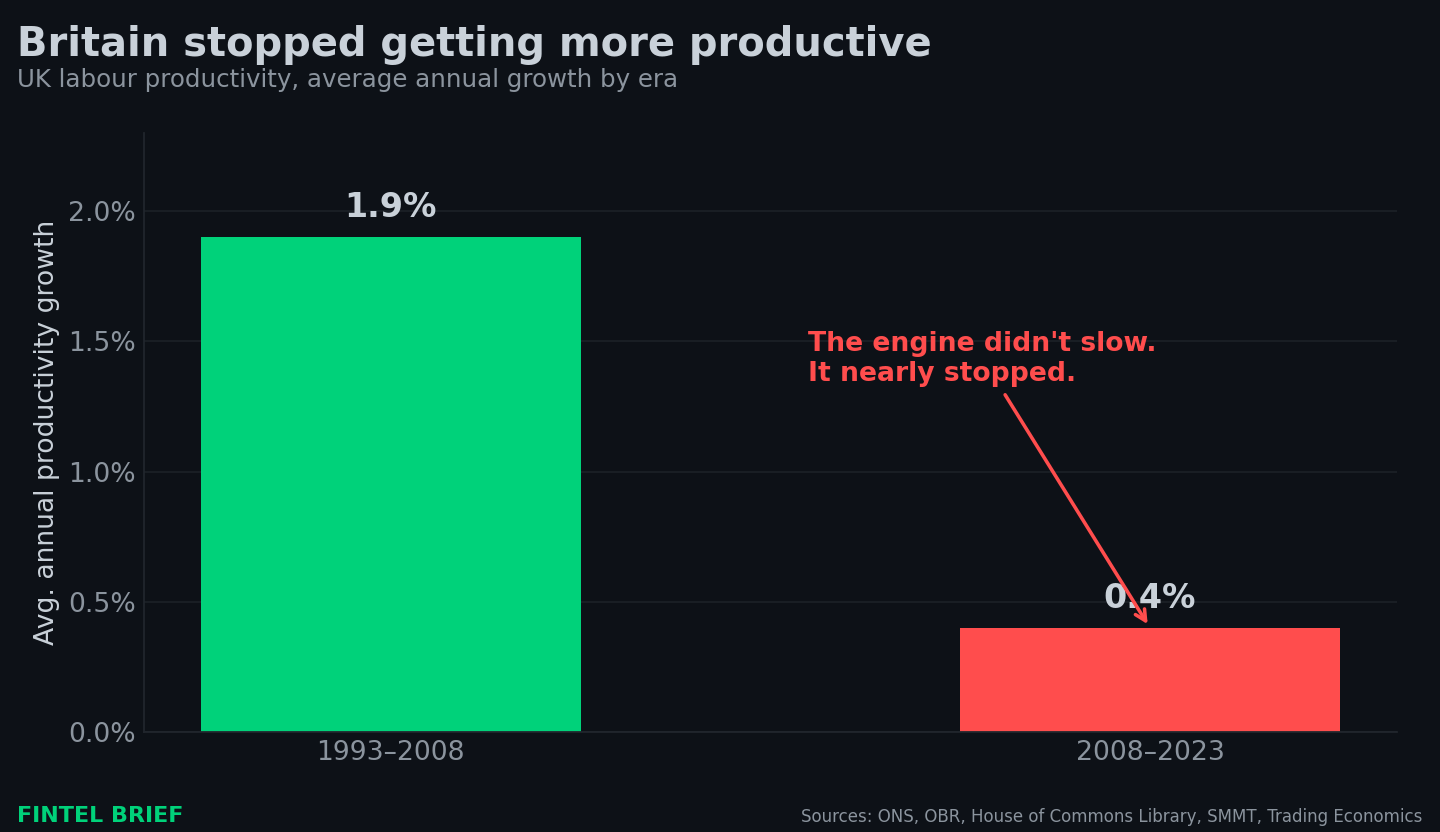

Begin with productivity, since it’s the only thing that makes a rich country rich. British labour productivity grew at an average of 1.9% a year between 1993 and 2008. From 2008 to 2023? Zero point four percent. The engine didn’t slow down so much as quietly seize up. An economy that stops growing output per worker has agreed, without telling anyone, to get poorer over time.

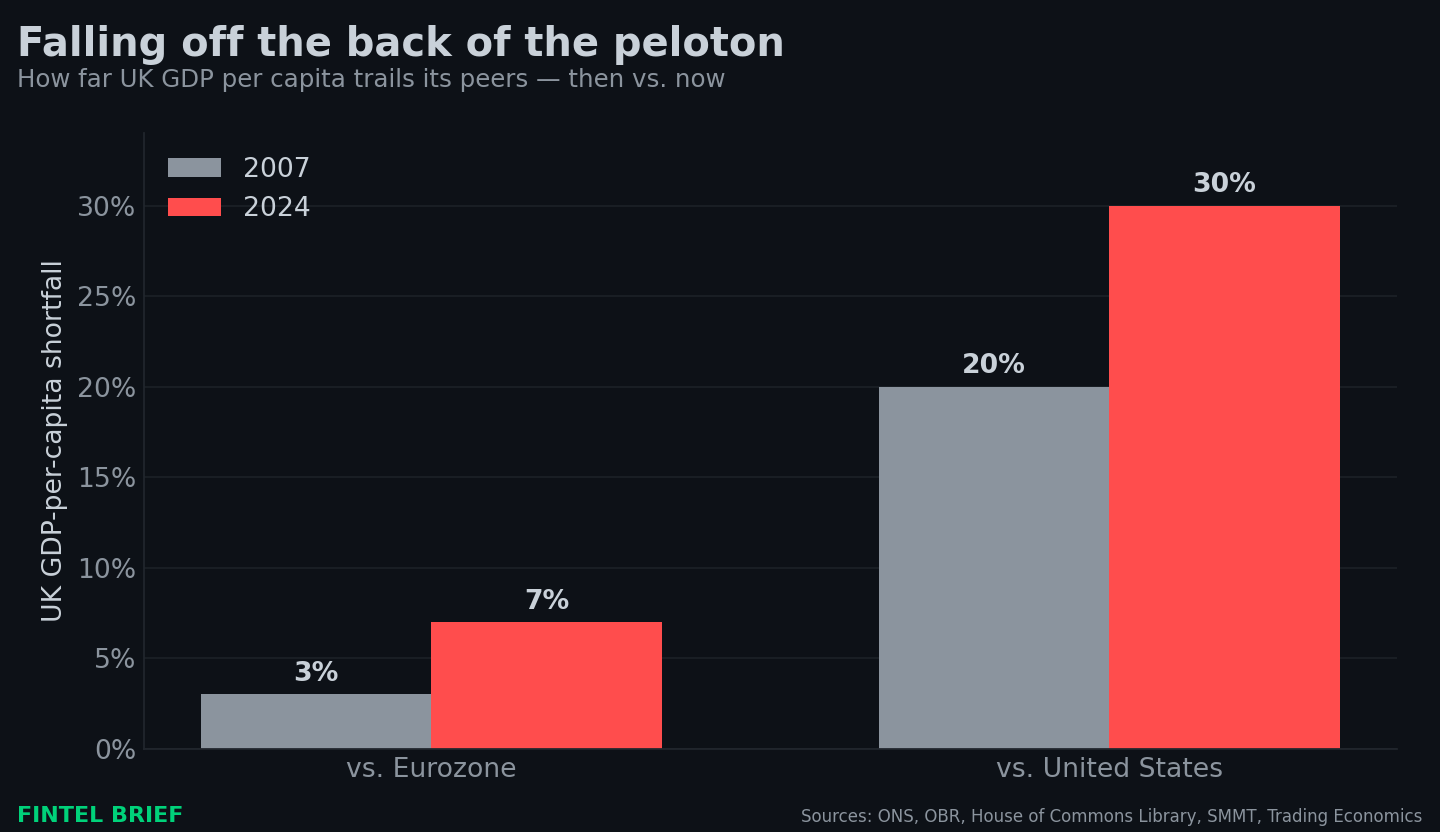

Then watch the living-standards gap widen in real time. In 2007, British GDP per capita trailed the Eurozone by 3% and the United States by 20%. By 2024 those gaps had blown out to 7% and thirty percent. Britain didn’t simply fail to catch America. It dropped off the back of the peloton and is now getting lapped. A whole G7 nation has spent seventeen years getting comparatively poorer and has marketed the experience as “stability.”

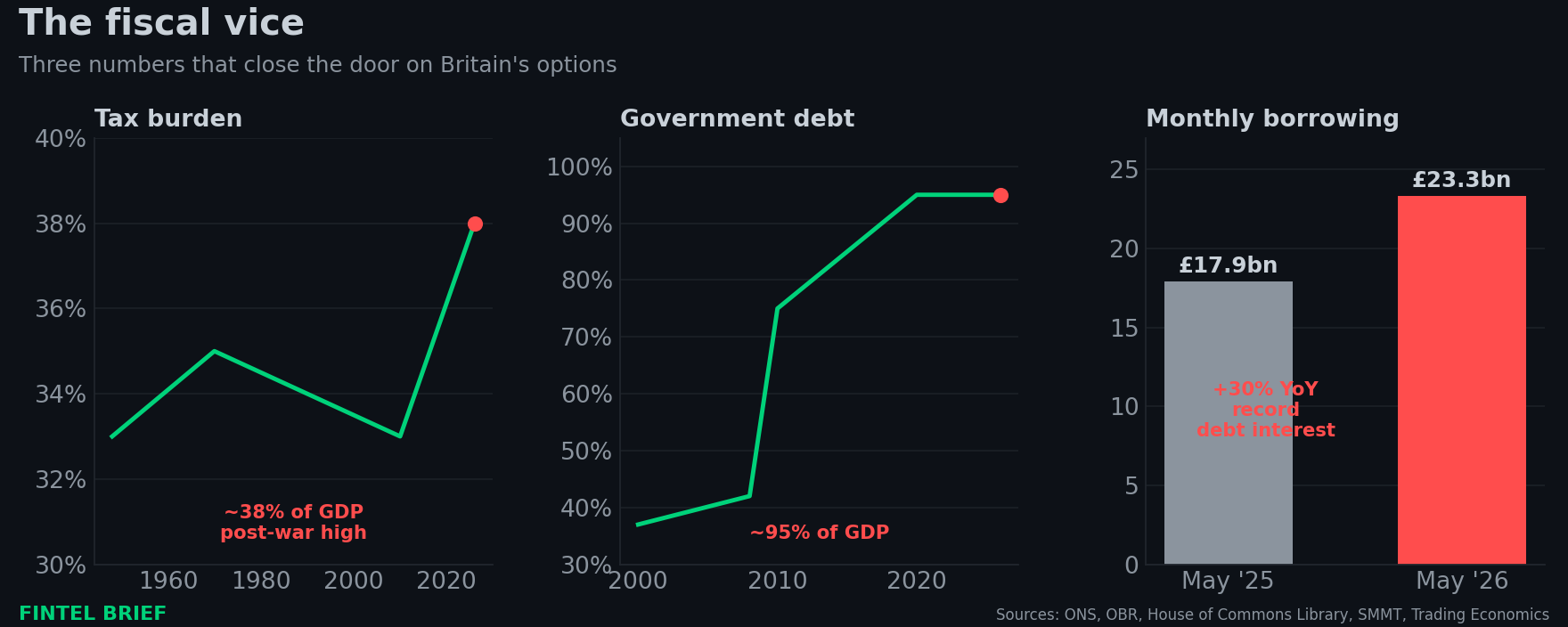

The public finances are the part that should bring on a cold sweat. Net borrowing is running north of 5% of GDP. Government debt sits in the mid-90s as a share of the economy. The tax take is climbing toward a post-war high of roughly 38% of GDP, which means the British state is now extracting more from its citizens than at any point since the rubble of 1945, and handing back stagnation in exchange. In May alone the government borrowed £23.3 billion, more than 30% above the same month a year before, as record debt-interest costs chewed through the budget.

Sit with that last one for a second. The fastest-growing line in the British budget is interest on money already spent. That’s the fiscal version of making minimum payments on a credit card while the balance quietly compounds behind your back. It’s about the most reliable warning light a sovereign has, and Britain has it flashing red.

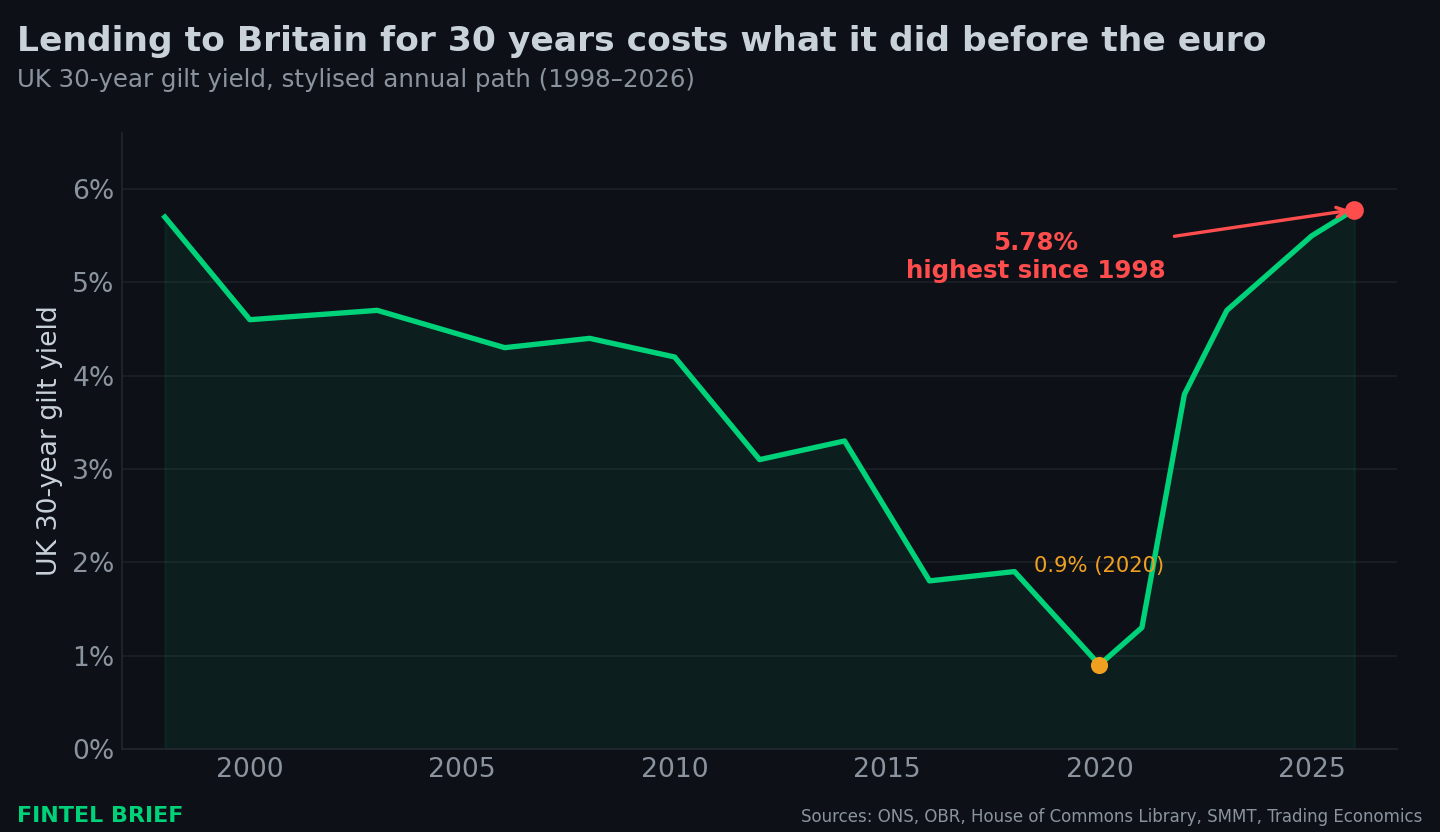

The bond market has clocked all this, even if the credit-default desk is still being polite about it. The 30-year gilt yield punched up to 5.78% this spring, the highest since 1998, a number that predates the euro itself. The long end of the British curve is saying out loud what the CDS desk won’t: lending to this government for thirty years now demands the kind of compensation last seen when Tony Blair was a fresh face.

So that’s the patient. Stagnant for a generation. Borrowing to cover the interest on its borrowing. Taxed to a post-war record with nothing to show for the receipt. Slipping behind its peers a little further every year that passes.

Part II: enter the mayor of the People’s Republic of Manchester

On the 19th of June they counted the votes in Makerfield, and Andy Burnham, mayor of Greater Manchester, a man who had to arrange a friendly MP’s resignation just to get himself back into Parliament, took the by-election with nearly 55% of the vote. He didn’t come back to the Commons to prop up the prime minister. He came back to bury him.

By the time you read this the knives are out in the open. Something like 97 Labour MPs have told Starmer to go. Cabinet ministers have walked. The betting markets make Burnham the runaway favourite to hold the keys to Number 10 by September. Starmer says he’ll fight. They always say they’ll fight.

So who is Andy Burnham, and why should a man who runs bus routes in Manchester trouble anyone with capital on the line?

Because Burnham looked at the economy we just described, the stagnant, over-taxed, interest-strangled patient, and concluded the real problem is that Britain hasn’t been spending enough.

His pitch, which he’s branded “Manchesterism,” promises to bring “the essentials of life” into public hands. Water, energy, rail. A 50p top rate. Capital gains taxed like income. Wealth taxes, land taxes, and a general conviction that Britain took a wrong turn somewhere around 1980 and ought to reverse the whole journey. His campaign manager designed Labour’s rail renationalisation. His allies are already naming names: the national grid, the regional electricity networks, the water companies, taken into “public control” one by one as they fail or their franchises lapse.

In fairness, and we do try to be fair, Burnham has spent recent weeks frantically reassuring the City that he respects the fiscal rules, that he never really meant the bit about ignoring the bond markets, that he won’t touch income tax or VAT or National Insurance. He is, by every account, a gifted shape-shifter.

But here’s the trouble with a man who promises to nationalise the water companies, respect the fiscal rules, and leave the only three taxes that raise real money untouched, all at once. The arithmetic doesn’t close. Something has to give. When the rhetoric of public ownership runs into the reality of an empty Treasury, one of two things happens. Either he breaks his word to the bond market, or he breaks his word to the activists who carried him there. There’s no third door, however much he’d like there to be.

The market has already worked this out. One FX desk we follow reckons a confirmed Burnham win nudges the euro higher against the pound on contact, and that the only genuine surprise left, the move that would actually jolt sterling up, is Starmer somehow surviving. Read that twice. The pound is now priced so that competent muddling-through is the bull case, and the base case is a man who treats the gilt market like a hostage situation he can negotiate his way out of.

This is what the end of credibility looks like. Not a default. A slow, polite, democratically-blessed rewriting of the rules the bondholders thought they were lending against.

Part III: the China trap, reloaded

Here’s where the two stories, the broke nation and the socialist mayor, fuse into something genuinely dangerous.

Give the Starmer government this much: on China it was at least competent in one narrow sense. It took the threat seriously. It seized British Steel back off its Chinese owner. It threw China’s state nuclear champion out of Sizewell and Hinkley. It forced Chinese stakes out of British chipmakers. Whatever you made of the warmth in Beijing, the security people kept a hand on the door.

Andy Burnham has shown none of those instincts. Not one, anywhere on the record.

His whole China history runs through his time as mayor of Manchester, and it reads like a tourism brochure for engagement. He led a trade mission to China. He launched a “China Dividend” report, at the British Embassy in Beijing, talking up the “golden era.” He praised Chinese high-speed rail. To this day he presides over a sprawling joint venture with a Chinese state construction giant at Manchester Airport. Asked about foreign policy, he’s said he wants to do the “bare minimum” of it. Let’s fix our own country first.

So put yourself in his shoes come autumn. You’re the new prime minister. You’ve promised reindustrialisation and northern jobs. You’ve promised public ownership you can’t pay for. The Treasury’s empty, the bond market’s hostile, and a Chinese battery-maker or EV giant turns up offering to build a gigafactory in a red-wall seat that hasn’t seen a real job since the pit closed. What does a jobs-first, security-indifferent, cash-strapped prime minister say to that?

He says yes. Of course he says yes. And the door the last lot kept one hand on swings wide open.

This is the dependency trap the optimists told us was overblown, and a Burnham government is precisely the thing that brings it back to life. Not because anyone sat down and planned it. Because a broke nation run by a man who treats foreign policy as a distraction will take the cheque every single time.

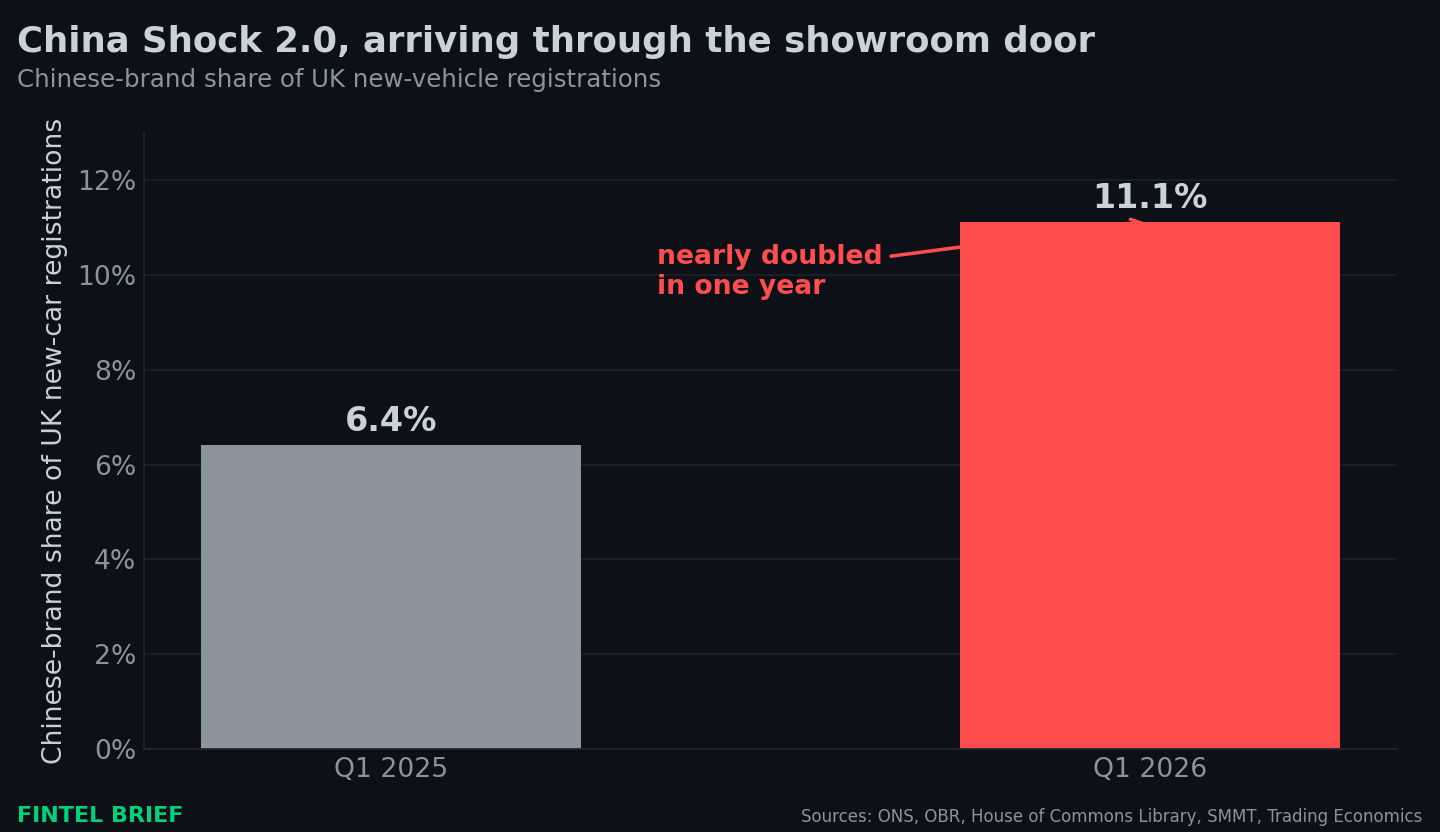

And he barely has to lift a finger, because the invasion is already coming through the front door of the showroom. Chinese car brands have gone from 6.4% of British new-car registrations to over 11% in the space of a year. BYD outsold Tesla in Britain last year. The single best-selling car in the country in one month this spring was Chinese. While the European Union was busy slapping tariffs and minimum prices on Chinese EVs to shield its own industrial base, Britain, open and broke and desperate for cheap goods to keep a squeezed electorate quiet, left the door ajar.

This is the same China shock that hollowed out German industry, and Britain has volunteered to go next, smiling the whole way.

We know what this dependency does to a country foolish enough to take the bet, because we’ve watched it play out across the manufacturing heartland of Europe in real time. The promise never changes. Market access, jobs, investment, a golden era. The delivery never changes either. A domestic industrial base competed into the ground, a strategic dependency that hardens into a geopolitical leash, and an endless, fruitless “dialogue” that produces communiqués and photo-ops while the factories go dark.

The market access never arrives. The dependency always does. That isn’t a forecast, it’s a pattern, and Britain is about to plant both feet on the exact spot where the trap is set.

Part IV: what we’re doing about it

We don’t write these pieces to ruin your afternoon. We write them to get you thinking. A thesis you can’t put into a portfolio is just a feeling, and feelings don’t compound. So here’s how we’re thinking about the trade. Not advice, never advice, just the way we’d lean if these were our own chips on the table.

We’re not short Britain. We’re short the idea of Britain. Roughly three-quarters of the FTSE 100’s earnings come from abroad, so a falling pound actually flatters those companies. It makes their foreign earnings worth more once they’re translated back into sterling. The pain in this story doesn’t live in the multinationals. It lives in the domestic mid-caps, the water companies, the grid operators, the banks geared to a home economy going nowhere. The cleanest way to express this is to separate the domestic from the international, rather than betting against an index stuffed with global oil majors and miners.

The contrarian “buy the panicked gilt” trade is, in our view, dead. A few weeks ago there was a respectable case that the fiscal fear had gone too far and the long bond was a screaming buy. That case died in Makerfield. You don’t step in front of a 28-year-high yield to buy duration in the same season a wealth-tax enthusiast moves into Downing Street. If anything the long end has further to climb, and the shape of the curve is where the cleaner expression sits: short rates pinned down by a central bank itching to cut, long rates impaled on fiscal risk.

Sterling insurance looks mispriced to us. When the market charges 15 basis points to insure against a sovereign credit event in a G7 nation that’s borrowing to pay its own interest and about to install a man who muses aloud about being “in hock to the bond markets,” you stop asking whether the event happens. You start asking how much of the insurance you can carry. Cheap convexity against a fiscal-credibility shock is the single most attractive line in the whole affair.

And we’re long the winners of the trap. If Britain is going to let Chinese industry compete its domestic base into the dirt while a Burnham government rolls out the red carpet, then the Chinese exporters and the broader China complex are, perversely, long the very force doing the hollowing. You don’t have to like it. You only have to notice who’s holding the knife.

The nationalisation candidates are the other side of that ledger, the listed water and energy names whose whole business model assumes the government won’t simply take them. When a prime minister tells you, on the record, that he means to bring “the essentials of life” under public control, the only sensible response is to believe him and price the equity accordingly.

Coda: the sound a great power makes

We opened on a sound. Let’s close on one.

It’s the sound of a prime minister’s plane idling on the tarmac in Beijing while a delegation of sixty files aboard clutching export brochures. It’s a 30-year gilt auction clearing at a yield nobody’s seen since before the euro existed. It’s a Manchester mayor, fresh off a by-election win, sharpening his lines about water companies and wealth taxes while the Treasury quietly drowns in its own interest bill.

None of those is a crash. That’s the whole trap. A crash would wake people up. What Britain is doing instead is the slow, dignified, democratically-sanctioned work of managing its own decline, and labelling each step “stability,” “reset,” “public control,” “a golden era.”

We named this piece for the Oxford man’s phrase because it’s perfect. The first fool’s golden era cost Britain a decade and a strategic dependency. The second is being negotiated right now, by a broke government about to be replaced by a broker one, with a man at the helm who thinks the bond market is something you can talk your way around.

You can’t talk your way around the bond market. You can only pay it, or break your promises to it. Britain is about to find out which.

We’ll be watching the gilt curve, and the cable.