Chinese influence into the global commodities markets

Getting the price you want is easy if you rig the markets

Key Judgments :

- Multiple Chinese firms were driving the price of nickel lower because China is the number one consumer of the metal

- There is a significant Chinese influence in the global commodities markets designed to manipulate the pricing of resources in favor of the CCP

- Similar to what was seen with Robinhood in the GameStop situation, brokers and exchanges will change the rules to appease certain institutions or nation-states

- Russia accounted for ~15% of class 1 nickel in 2021, and the war in Ukraine will disrupt shipments and mining operations for the foreseeable future

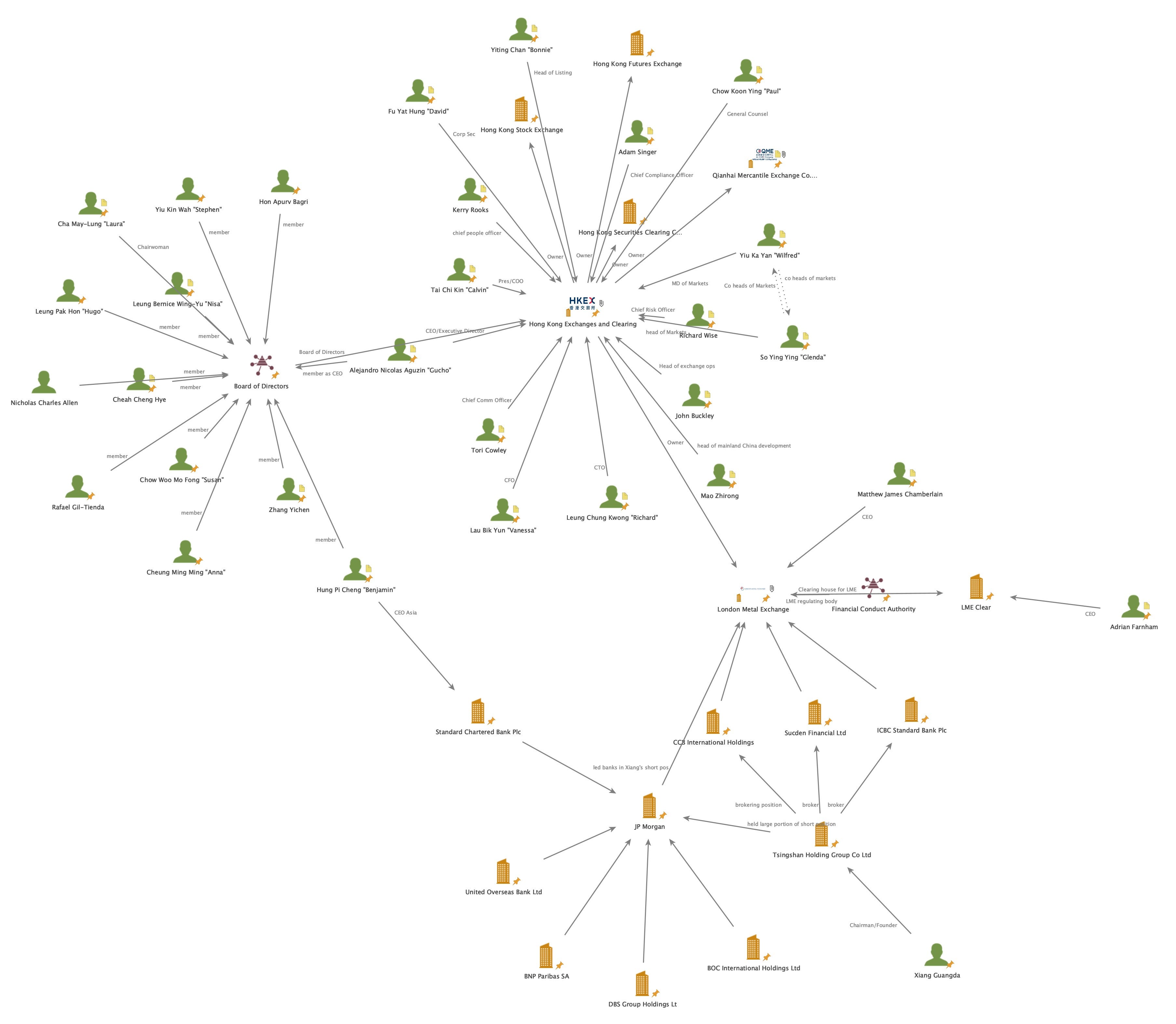

The recent events in the London Metal Exchange show a significant risk to investors who are not tied in with the Chinese Communist Party. A primary concern is its suspension of nickel trading and retroactively canceling all the transactions on the morning of March 8 as prices doubled. The short squeeze in nickel started by Xiang Guangda and his Tsingshan Holding Group Co Ltd has shown weakness in the LME and collaboration and corruption between the Chinese Communist Party and the commodities markets worldwide.

It is a well-known point that Hong Kong is no longer a tacitly controlled piece of the Chinese mainland. They are now fully locked into the CCP’s control. Understanding this and looking at the ownership structure of the London Metals Exchange shows us that they are owned by a Hong Kong firm, HKEX (Hong Kong Exchanges and Clearing). This group also owns The Hong Kong Stock exchange, Futures exchange, Securities Clearing Company, and the Qianhai Mercantile Exchange, a mainland China commodities exchange.

The short squeeze stopping the LME was designed to squash the nickel price for the largest consumer of nickel (China) to capitalize on the delivery price. When the invasion of Ukraine kicked off, and with Russia providing a sizable portion of nickel to the world, the costs would rise drastically, forcing Xiang to cover his losses. The relationships, both formal and informal, previously mentioned allowed the Chinese and Xiang to stop what would have been an $8 billion loss and potentially more.

Counterparty risk is the probability that the other party in an investment, credit, or trading transaction may not fulfill its part of the deal and may default on the contractual obligations.

Most of Xiang’s short positions were through derivatives with major international banks giving him leverage for bigger positions. An increasingly more complicated derivates market increases the risk as well as the likelihood of collusion and corruption in exchanges and markets. Risk managers can only manage risks they are aware of and in situations like this Xiang and his firm seem to have intentionally covered up their position sizing so as to not raise any risk officer or regulators’ concerns. The FCA (Financial Conduct Authority) which is the regulator for the LME has a lot of regulatory controls they can put in place however its worth noting that they also have a great relationship with the CSRC (China Securities Regulatory Commission) and a partnership in the Shanghai-London Stock Connect

The Shanghai-London Stock Connect is a landmark in cooperation between UK and China in the sphere of financial markets. The programme will strengthen connectivity between UK and China capital markets, deepen capital markets in both countries and enhance the status of Shanghai and London as global financial centres, to the mutual benefit of both countries.

This is a sign of the trend that started with Robinhood limiting order flow out of positions that were being squeezed such as Gamestop and AMC during the pandemic due to not having the shares to sell and being stuck in synthetic positions. When the LME closed the nickel markets for over a week to avoid angering China and causing Xiang to lose billions they showed that they similarly answer to whoever pulls their puppet strings. in the Robinhood example, it was Citadel, in this example, it’s the CCP. Normally it is impossible in physical commodities markets to create synthetic shares because you have to be able to deliver the physical goods on the orders entered or provide cash settlement. However, it seems Xiang’s positions across multiple banks and brokers were so overlooked that no single risk manager would raise an eyebrow at the positions.

Brooooo… these keep getting better