China's Dominance in Shipping: The Implications for Global Logistics and U.S. Preparedness

China's Dominance in Shipping: The Implications for Global Logistics and U.S. Preparedness

Addressing China's Growing Grip on Global Shipping and Navigating Challenges in a Monopolized Maritime Era

For decades, the azure waters of the Mediterranean echoed with tales of Greek maritime prowess. Long before the meteoric rise of China in the global shipping arena, Greece, with its rich nautical heritage, held sway over a significant portion of the world's maritime trade. Leading Greek shipping conglomerates, such as Danaos Corporation ($DAC) and Diana Shipping Inc. ($DSX), were not just household names in the Hellenic Republic but were also traded as industry titans on the international stage. Their fleets traversed every major shipping lane, bearing goods that powered economies and connected continents. However, the winds of change have since shifted, and as the world transitioned into the 21st century, Greek dominance began to encounter formidable challenges from the East.

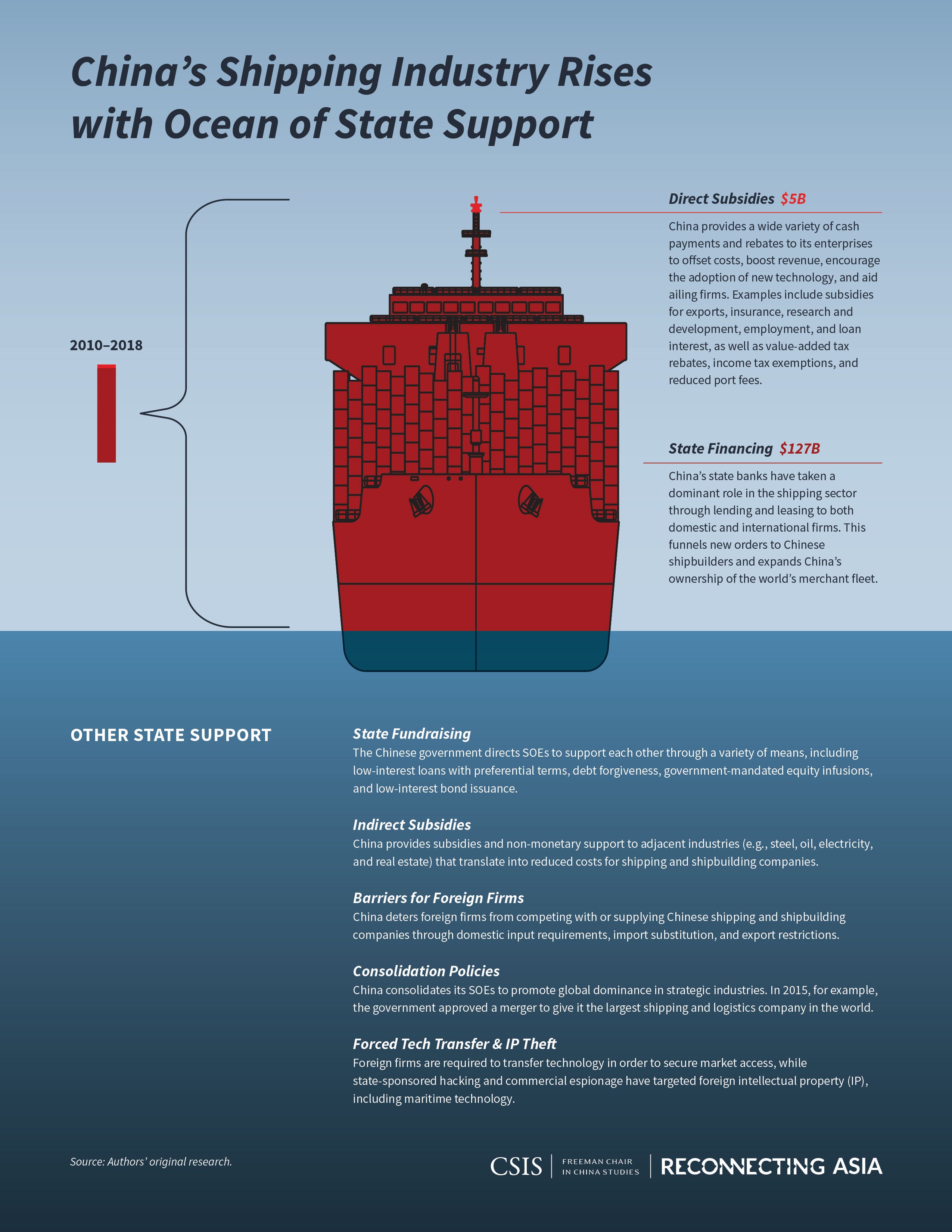

The evolution of China's shipping industry is grounded in the CCP’s ability to subsidize their corporations to lower costs for external customers and starve competition. From the beginning, China has deftly navigated its way to the forefront of global shipping, leveraging its vast manufacturing base and strategic investments. But as China's maritime star rose, the longstanding Greek shipping luminaries found themselves in an increasingly competitive and complex global landscape. The story of this transition is not just about ships and trade routes; it's a reflection of broader geopolitical shifts and the reshaping of global economic dynamics.

The world of shipping is witnessing a seismic shift. Suppose recent data from various sources are any indicator. In that case, China and Chinese banks are swooping up most tanker and shipping vessels with its rapid climb to the top regarding ship ownership and its seemingly unassailable position in container manufacturing. For example, The top three Chinese companies make 86% of the world's intermodal chassis and produce 95% of global containers, including those used for U.S. trains and trucks. The Middle Kingdom stands tall, casting a long shadow on supply chains and geopolitical tectonics.

China's rise in the shipping sector has been nothing short of meteoric. A report from Clarkson Research Service recently revealed that China, riding a tide that began around 2015, now surpasses Greece in gross tonnage, owning a 15.9% market share. This is no minor feat. While Greece maintains an edge in deadweight tonnage, the symbolism of China's ascension is hard to miss. It represents more than just numbers. It's emblematic of China's growing clout in the global economy.

But this is just the tip of the iceberg. More than 95% of the world's containers are produced in China, as per maritime consultancy Drewry. For those outside China, this presents an undeniable vulnerability in the supply chain. Imagine a scenario where geopolitical tensions, especially with the country’s increasing threats toward Taiwan’s sovereignty, intensify. The heavy reliance on China for steel containers could precipitate an unprecedented supply chain crisis, further exacerbated by disruptions like the ones witnessed during the COVID-19 pandemic.

The U.S. especially should sit up and take notice. As Carl Bentzel from the Federal Maritime Commission rightly pointed out, China's dominance in container production is essentially a "monopoly" of "an essential product." Any disruption here would ripple through global trade like a tidal wave, leaving economies floundering in its wake. Although steps are being taken to mitigate this risk, with manufacturers exploring opportunities in Vietnam, India, and US domestic production, the sheer scale and efficiency of China's output cannot be replicated overnight.

Yet, there's more. The tanker industry, the lifeblood of global oil transport, is also vulnerable to China's economic ambitions. China's insatiable appetite for oil has made it a pivotal player in the tanker industry. And notably, the oil they get from sanctioned Russian firms. But with China’s Finance Minister hinting at a potential GDP growth slip below the 7% mark, there could be implications for oil shipments. A slowdown in China's economy could lead to reduced oil shipments, impacting tanker companies worldwide. Companies like Teekay Tankers ($TNK), Nordic American Tankers ($NAT), and others might feel the squeeze if China's economic momentum slows.

But what does this all mean for the world, especially the U.S.? It is clear that China's maritime ascendancy, both in terms of ship ownership and container manufacturing, underscores a strategic vulnerability for many nations. In an era where supply chains have become more crucial than ever, the U.S. and its allies must reassess their dependencies. The emphasis should be on diversification and reducing the risks associated with over-reliance on a single dominant player. The recent sanctions on Raytheon and Lockheed in China by the CCP are having immediate effects on specialty shipping containers needed to supply missile defense systems to INDOPACOM. A move that will have large-scale strategic repercussions at a time when the US government is not able to spend its way out of problems.

Washington's push for "smart containers" with tracking technology is a step in the right direction, but it is just the beginning. More needs to be done to encourage container manufacturing outside of China and to bolster the global tanker industry against potential economic downturns in key markets. The Chinese juggernaut in the maritime world isn't just about ships and containers; it's about global economic dominance “with Chinese characteristics,” as Xi likes to explain it, and ensuring that only China holds disproportionate sway over global trade arteries. As we navigate these uncharted waters, prudence, foresight, and strategic recalibration will be essential. The world cannot afford to sail blindly into a storm.

Well done