China’s Dollar Oxygen Problem

China’s dedollarization master plan missed the moment because the real world rewards liquidity, not promises

If you need more on this check out some of my related work “The Girl From Ipanema Walks… Straight Into a Debt Snowball” and “Solvency is a Theory. Settlement is a Fact.”

“If it don’t make dollars it dont make cents (sense)” - 50 Cent (probably)

There’s a popular macro story making the rounds that goes something like this:

“Oh no the sky is falling. The dollar is being debased and the rest of the world is finally getting serious about alternatives.”

This started with a JP Morgan report in June of ‘25 and from then on its been making its rounds in the news and on X with everyone who gets clicks and views from doomsday prophecies for America.

“Dedollarization” becomes the banner under which every incremental change gets interpreted as a huge geopolitical shift. I think that is completely wrong, and shows that finance is not immune to people trying to just go with vibes as an investment strategy.

The ACTUAL thing that decides regimes in real time is not a speech, a summit, or a headline about “moving away from the dollar.” It’s the plumbing. It’s the unglamorous machinery underneath global trade and finance:

cross-currency basis

collateral acceptance

repo and offshore funding

bank balance sheet capacity

who gets dollar liquidity in stress and who doesn’t

When volatility rises, the reserve currency doesn’t politely step aside. It tightens. It concentrates. It behaves less like a public utility and more like a gated community.

So here’s the thesis I want to put out there:

China’s structural access to U.S. dollar liquidity is still something they need and it has deteriorated enough that it now behaves like a system constraint.

The pipes have begun to bifurcate.

China is compensating with workarounds—gold-linked funding, indirect channels, improvisation—and those workarounds are showing up as premia and distortions.

The stress is not staying inside China. It’s pushing outward into emerging markets, with Brazil sitting in the highest-pressure part of the apparatus.

I call it China Liquidity Asphyxiation.

That word—asphyxiation—is intentional. This isn’t “China is weak” or “China is doomed.” It’s more specific and more mechanical

In the modern system, USD liquidity is oxygen.

You can dislike that. You can plan for a future without it. You can build parallel rails at the gov to gov levels and tell everyone its really going to happen. But if you’re short oxygen before you hit the surface, the lights start to close in.

And timing is exactly where China’s dedollarization narrative is most vulnerable.

The end of China using the USD is happening before they have a trusted system in place to replace it.

For roughly two decades, the global economy ran on a simple symbiosis:

China exported deflation: cheap manufactured goods that lowered global CPI

and recycled its surplus into U.S. Treasuries: cheap capital that lowered global yields

That engine let’s call it “Chimerica,” (open to better names) or call it globalized disinflation. It softened cycles. It made risk feel manageable. Now that engine is stalling.

What’s replacing it isn’t a neat transition from Dollar World to Multipolar World and all of the think tank reports have already beat those words to death. It’s something uglier: segmentation. The world is splitting into inside-the-wall and outside-the-wall access to the dollar system, but the dollar system still reigns supreme.

And if you want to understand why I think China’s de-dollarization pivot has missed the moment, you need to see where the segmentation is showing up.

If you come for the King Dollar you best not miss.

Five Structural Fractures

I’m going to keep this grounded: five observable fractures, each pointing in the same direction. You can disagree with the conclusion, but the point is that these are not vibes-based claims.

Each fracture is best understood as a test of one question:

Can China reliably transform its assets and claims into usable USD liquidity under stress?

The answer, in the data we’ve examined, is increasingly: no. Because they still do need USD regardless of what Xi and the CCP think, their companies and national champions are all addicted to it, and it is still the default internationally.

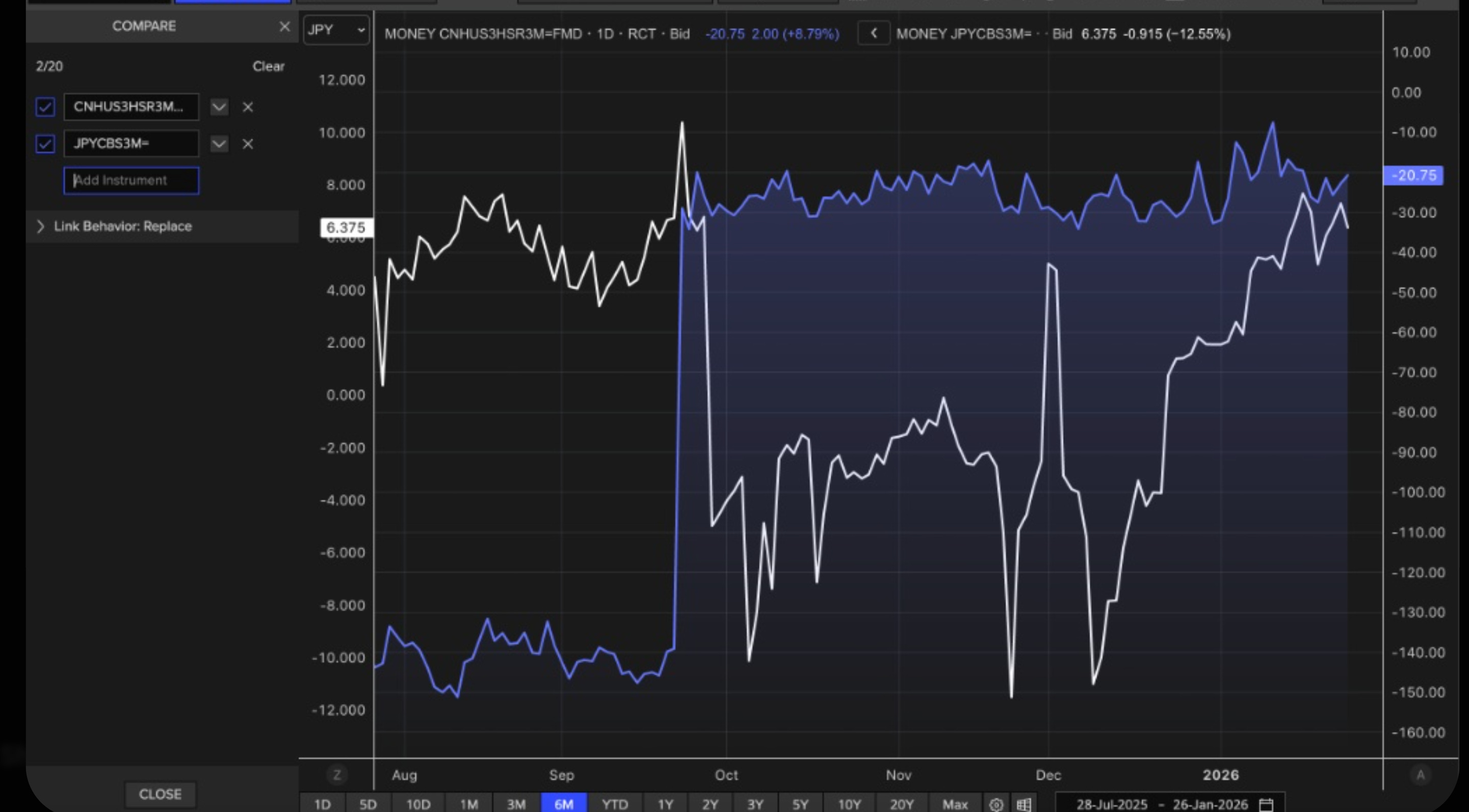

1) The Ring-Fence

Direct access denied.

Historically, Japan has acted as the dollar wholesaler for Asia. Because Japanese megabanks (like MUFG and SMBC) hold massive amounts of US collateral (Treasuries/CLOs) and Japan benefits from the BoJ–Fed swap line architecture and deep USD/JPY funding markets, they effectively import raw dollar liquidity from the US and re-exported it to the region. Chinese state banks would use the deep JPY/USD Cross-Currency Basis Swap market to access this pool. Instead of begging for dollars in New York (where political scrutiny is high), they would swap RMB for JPY, and then use the liquid Tokyo market to swap that JPY for USD. For decades, this trade was driven by the Yield Differential. China’s 10-year yields were significantly higher than Japan’s (often 3% vs. 0%), creating a natural gravity that pulled Japanese surplus capital into China.

So the cross currency basis, in simple terms, tells you how expensive it is to swap into dollars via the market. When balance sheets are healthy and intermediation is working, all is well. When intermediation is constrained, by regulation, risk aversion, policy, or counterparty stigma, basis starts to act as a pressure gauge.

When basis stays stressed, you’re looking at a market that’s telling you—quietly, persistently, The usual Chinese pipe to USD has a problem.

Implication: Asian liquidity has been partitioned.

Japan is inside the wall.

China is outside the wall.

If you’re trying to understand how dedollarization intersects with reality, this is a good first checkpoint: a genuine shift away from the dollar shouldn’t coincide with a sustained market premium for accessing dollars through the plumbing.

2) The Euro-Stop

Credit contagion, de-risking, and the retreat of conduits.

Signal: A sharp spike in Standard Chartered CDS when liberation day was announced in April.

CDS (Credit Default Swaps) is the market pricing the risk of default and distress, similar to buying insurance. So we can look at the banking layer, specifically the conduits that historically help intermediate trade and funding across regions. The key takeaway from that chart is when CDS spiked the equity sold off to the tune of 30%

Why care about a bank CDS chart? Because HSBC and Standard Chartered are how China gets USD from the UK system. When a conduit’s risk pricing jumps, you’re often looking at more than “credit.” You’re looking at expectations about second-order effects like reduced unsecured lines, higher haircuts, tighter terms, and less willingness to warehouse risk.

Liquidity usually doesn’t vanish with an announcement. It thins out through behavior. CDS spikes are one of the market’s cleaner ways of telling you behavior is changing.

In practical terms: Everyone has been de-risking in regards to China for the last 2 years. if European conduits begin de-risking China-linked exposure, especially unsecured lines, then dollar access gets narrower at exactly the wrong moments, and “workarounds” become more important, more expensive, and more visible.

Standard Chartered is in a similar boat as HSBC. They are the other channel through which global trade and finance flows between regions. When conduit risk reprices abruptly, it’s a sign that private-sector participants are pulling back from unsecured exposures that depend on stable cross-border conditions.

Implication: European banking conduits have begun to quantify risk associated with China-linked liquidity exposure. Particularly the kind that matters most in stress: unsecured lines, wholesale funding, and cross-border intermediation. So this will impact the CCP’s ability to get liquidity when they need it as the stress of trying to move off the dollar becomes worse.

Think of it this way: the system doesn’t need an official “ban” to shrink liquidity. It just needs the internal risk committee to say, “Not at this price.”

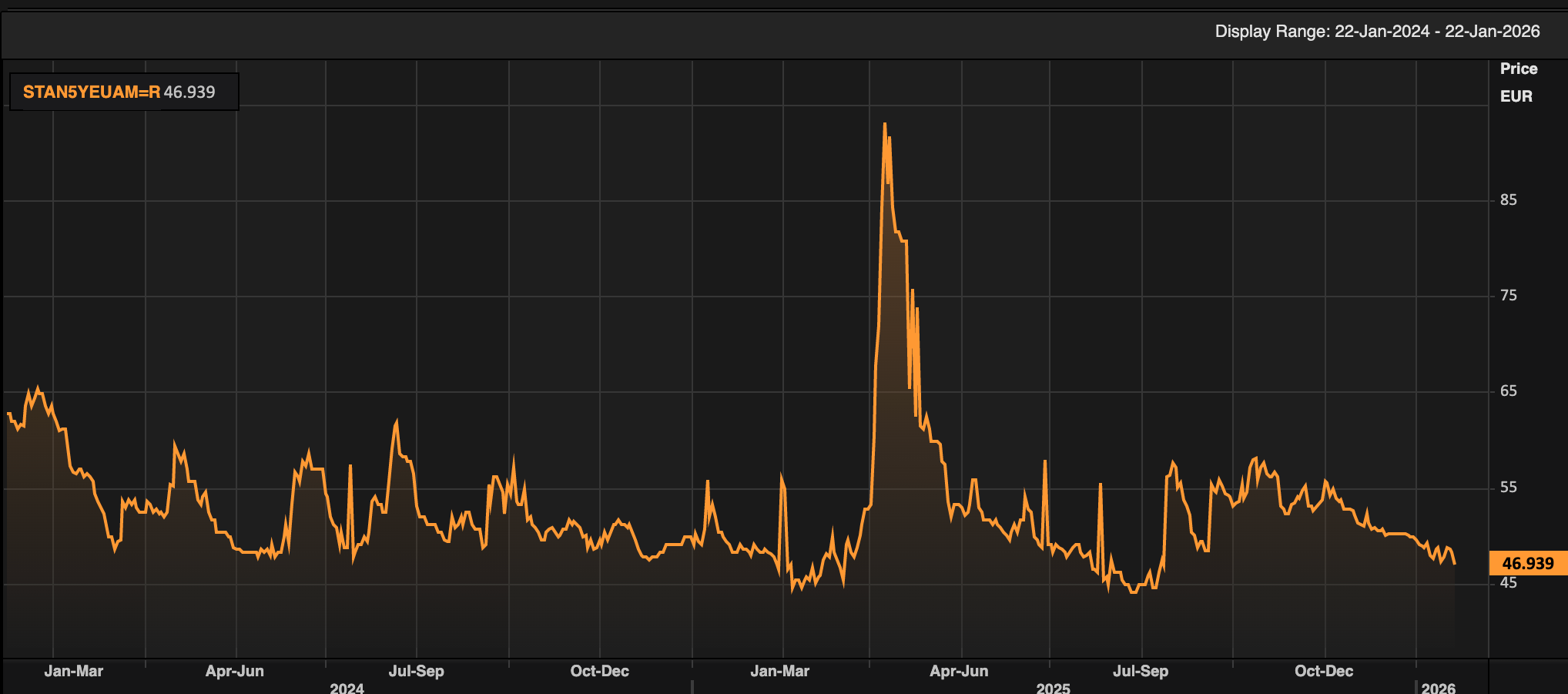

3) The Shadow Premium- The Gold Part

The third fracture is the one I think everyone has been talking about recently and thats China’s massive gold purchases, both for the last few years and for the last 15 years using the BRI gold for investment plays in Africa.

Gold is behaving like an escape-hatch asset in a tightening liquidity regime. The purest version of this is the implied funding premium; here’s a proxy chart that shows the same behavioral shift.”

Put plainly the market is showing a meaningful premium for obtaining synthetic dollar liquidity through gold-linked pathways relative to clean benchmark funding.

This chart is a blunt proxy (price vs rate), but it captures the same behavioral shift: gold is being treated less like a commodity and more like a funding/settlement escape hatch. Everyone knows China wants to back something with gold, but the going assessment is that it will be small and selective. This chart doesn’t happen in a world where the banking pipe is wide open. It happens when some actors prefer—or are forced—to source dollars through nonstandard channels.

If you believe the “dollar is irrelevant now” narrative, this is awkward evidence. The price behavior is more consistent with a world where dollars are still the dominant settlement asset in stress, and access is getting more conditional.

I’m not arguing that gold is magic. I’m arguing that when you see gold become a more prominent funding bridge, it’s often because someone is operating around the conventional system rather than inside it.

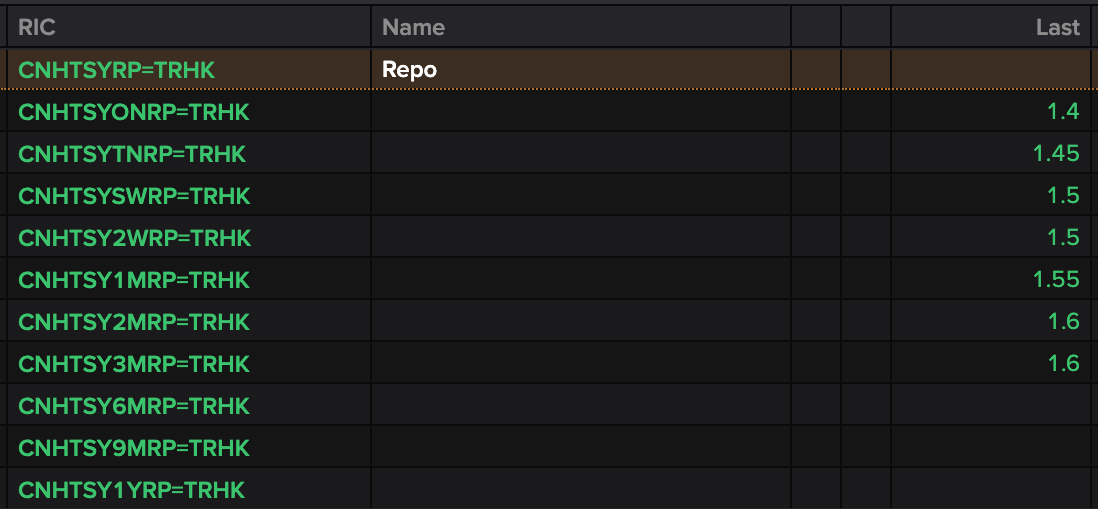

4) The Ghost Collateral

Signal: A “null signal” in offshore repo (TRHK): stuck around ~1.4% while USD funding sits much higher (~4.2% in the comparative snapshot).

This is the most technical fracture, and it’s also the most important for understanding why systems snap.

Repo is where collateral becomes money. In normal times, if an asset is treated as high-quality collateral, it should fund smoothly and reprice in line with comparable benchmarks. In segmented systems, collateral becomes “local”: accepted here, discounted there, refused somewhere else.

In the slice we reviewed, the offshore repo signal we tracked (TRHK) looked pinned in a way that didn’t map cleanly to USD benchmarks—sitting far below USD funding rates in the comparison snapshot.

The “stuckness” is the tell. It suggests RMB liquidity is circulating inside a silo rather than converting cleanly through global collateral channels. Another way to say it: some balance sheets appear to treat Chinese collateral as less money-like when you need it to behave like money.

That matters because collateral acceptance isn’t just a technical detail; it’s the gateway between “I have assets” and “I have funding.” especially when you have been trying to move the BRICS off the dollar for 6 years or more.

Western balance sheets appear to be treating Chinese Government Bonds as non-money-like in the contexts that matter: offshore funding, stress convertibility, and reliable transformation into USD liquidity. That’s why I call it ghost collateral. The paper exists. The “value” exists on a screen. But in the one place that matters—turning assets into funding—its usefulness fades.

China wants to remove themselves from the USD, but no one trusts them, so they can’t.

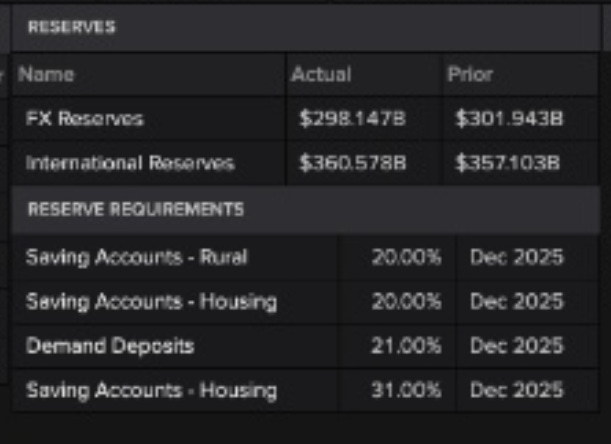

5) The Brazilian Limit

If you only remember one part of this framework, remember this: Brazil is where the mismatch becomes measurable. In the data we examined, Brazil’s cash FX reserves were drawing down at roughly $3.3B/month.

Reserve levels are a constraint variable. Reserves determine how much volatility a country can absorb before policy options narrow: the ability to smooth FX moves, defend a currency, maintain confidence, and avoid forced adjustments. Brazil functions as a kind of absorber: it is large enough and connected enough to warehouse parts of the settlement mismatch thus holding exposure that isn’t as liquid as USD while bleeding USD in the process.

Brazil’s Lula told China they would work in Yuan, but everyone in Brazil who owns a business or likes not turning into Argentina wants USD. So in order to conduct commerce Lula has to draw down dollar reserves, which his government doesn’t want to do business in anymore. If the drawdown persists and volatility rises, you can model a runway. Using a conceptual “safety floor” around $250B, the path points toward a higher-risk zone around Q4 2026.

I’m not calling the day. I’m calling the constraint. As the runway shortens, the probability of a forced adjustment rises, even if the specific trigger is unknowable.

Why this makes dedollarization look late—not early

This is where I part ways with the loudest version of the “dollar debasement” crowd.

If the dollar were simply fading into irrelevance, you’d expect stress premia for accessing dollars to compress, not persist. You’d expect the global collateral machine to become more substitutable, not less. You’d expect cross-currency basis to behave as the market migrates away from the dollar.

Instead, multiple independent signals point toward a different reality:

access to USD liquidity looks more conditional

alternatives look more expensive at the margin

collateral transformation looks more segmented

and the spillover is showing up in places like Brazil

That’s why I think China’s dedollarization pivot has missed the moment. It’s trying to lean away from the system at the same time the world is repricing the system’s liquidity as strategic.

If the plumbing is bifurcating, the global macro outcomes tend to become binary. Not because the world is simple, but because segmented systems don’t glide. They snap.

I see two broad scenarios.

Scenario A: The Hard Stop

In this path, shadow liquidity workarounds don’t scale fast enough to offset narrowing access through conventional channels. At some point, a funding wall becomes real, not necessarily because of a single policy announcement, but because enough private balance sheets stop providing the marginal intermediation.

How it shows up:

USD spikes as the settlement asset everyone wants becomes scarce at the margin

commodity prices weaken in USD terms as marginal demand loses financing oxygen

EM balance sheets tighten as USD liabilities and funding costs reprice

contagion risk rises through index-linked channels, especially if a large EM is forced into adjustment

European banking stress becomes plausible if conduit risk morphs from “credit concern” into “funding concern”

This is the path that looks deflationary after the initial shock. Risk assets get repriced lower, and the scramble for liquidity dominates everything else.

Scenario B: The Shadow Valve

In this path, China succeeds—partially—in keeping essential flows moving through alternate arrangements and workarounds, even as conventional pipes deteriorate.

The system doesn’t “normalize” here. It splits into two blocks that can interact, but with more friction, more premia, and more reliance on neutral settlement bridges.

How it might get there:

less recycling of surpluses into U.S. duration implies higher yields to clear financing needs

the old disinflationary loop weakens, making inflation stickier in the West

global trade becomes more block-structured

gold’s role as a neutral settlement bridge becomes more prominent (and the funding premia we see make more sense)

This is the path that looks stagflationary: less growth certainty, more inflation persistence, higher volatility.

Brazil is the fulcrum

Brazil is not a footnote in all of this and a lot of it will come down to Lula.

Brazil sits in EM indices, is widely held, and is liquid enough to become the “sell button” when global funds face redemptions. That’s why reserve trajectories matter, they influence not just domestic policy, but the probability of an event that forces global portfolios to react.

A simple tell I keep coming back to is the CNY/BRL cross alongside reserves. Cross-rate stress paired with reserve drawdown is often how balance-sheet reality shows itself before policymakers start explaining it. If the cross moves while reserves fall, the subsidy is unwinding.

Portfolio implications: win from disorder, not perfection

When a system bifurcates, portfolios built for a single smooth outcome tend to suffer. You don’t need a perfect forecast; you need exposures that survive a range of unpleasant regimes.

The “wins in multiple paths” bucket here is volatility and settlement-neutral hedges.

Long gold volatility is attractive in both broad scenarios: in a hard stop, it benefits from stress and liquidity hoarding; in a bifurcation path, it benefits from gold’s role as a neutral bridge and from the persistence of premia.

Be careful with fragile conduits (especially European financial plumbing that’s sensitive to Asia-linked stress) where a credit issue can become a funding issue quickly.

The watchlist: five live indicators that decide the thesis

If you want to track this like an operator, not a pundit, here’s the dashboard:

CNH basis vs JPY basis (ring-fence)

Conduit bank risk pricing (euro-stop)

Gold-linked implied funding vs SOFR (shadow premium / “alligator jaws”)

Offshore repo behavior & collateral acceptance (ghost collateral / null signal)

Brazil FX reserves + CNY/BRL cross (Brazilian limit / clock)

The dollar isn’t weaker in stress it’s stronger

If you believe the dollar is being debased into irrelevance, then China’s dedollarization push looks like history moving forward.

If you believe the world is entering a liquidity-first regime like I do, then China’s pivot looks riskier, because the pivot is happening as the pipes tighten.

My view is blunt:

The next regime doesn’t reward the most elegant narrative.

It rewards the currency that still clears, the collateral that still finances, and the balance sheet that still intermediates in stress.

That remains the dollar system.