Ample Reserves, Ample Alibis

Reserve “management” is the new QE until the long end decides it isn’t.

First off Merry Christmas, happy holidays, hope everyone has had a good year. a great year even.

“The first lie in macro is that labels matter more than flows.”

We keep hearing that nothing is happening. The Fed isn’t easing, just “maintaining ample reserves.” Treasury isn’t pulling demand forward—just “optimizing issuance.” Regulators aren’t loosening, just “improving market function.”

And yet the pipes are widening in three places at once. When that happens, money doesn’t debate philosophy. It moves.

So here’s the 2026 question we can actually trade: what is the market still pricing as a one-off technical tweak, even as the U.S. policy stack is quietly re-engineering liquidity?

The setup

Start with the observable facts.

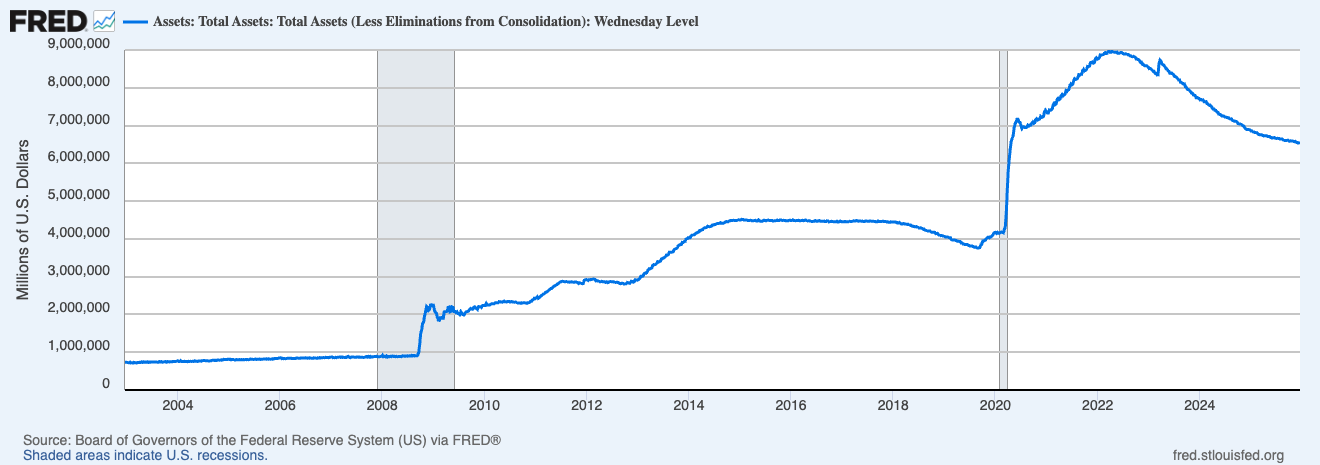

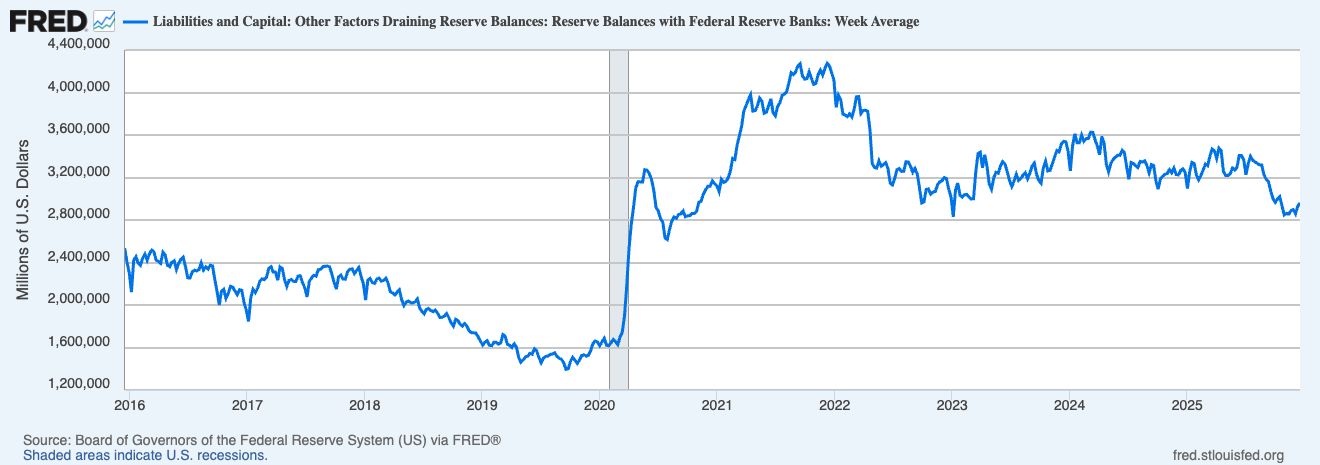

On December 10, 2025, the Fed cut rates and—more quietly, more importantly—laid the groundwork for Reserve Management Purchases: buying short-dated Treasury bills to keep reserves ample and keep control of money-market rates.

The NY Fed spelled out the opening bid: the first schedule (released Dec 11) totals ~$40 billion of bill purchases starting Dec 12, with monthly amounts communicated going forward. This is where the semantic games begin. Chair Powell’s line—supported by every central banker’s instinct for self-preservation—is that this is “technical,” not a shift in stance. Fine. But mechanically it increases the balance sheet and adds reserves. The flow is the story, not the label.

Now zoom out to Treasury. Treasury has already telegraphed a willingness to lean more heavily on bills (and the refunding process is where that posture gets expressed and adjusted). The next key waypoints are February: documents on Feb 2, 2026 and the quarterly refunding announcement on Feb 4, 2026.

Finally, the regulators. The FDIC and other agencies finalized changes to the enhanced supplementary leverage ratio framework with an effective date of April 1, 2026 and optional early adoption January 1, 2026, a direct nod to the fact that leverage constraints can discourage Treasury intermediation.

Put differently: the Fed is adding reserves, Treasury is leaning short, and banks are being given more balance-sheet oxygen. That combination doesn’t automatically create productive investment. What it reliably creates is refinancing capacity. And refinancing is where the mispricing lives, because it changes credit outcomes without changing growth narratives.

What this is NOT

This is not a call for monetary apocalypse. We’re not doing “currency collapse” fan fiction. We can leave that to the Peter Schiff’s of the world

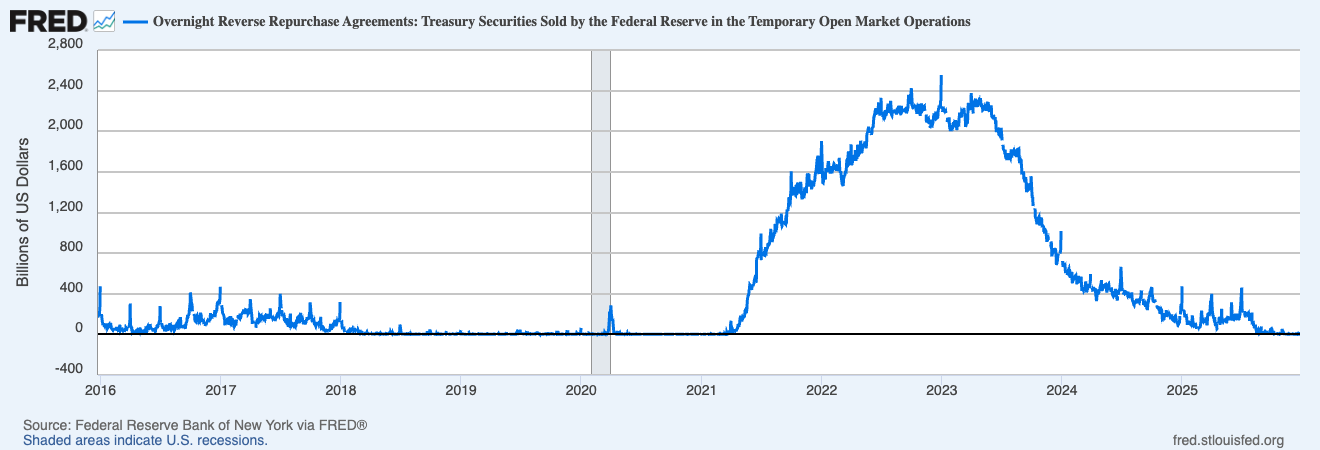

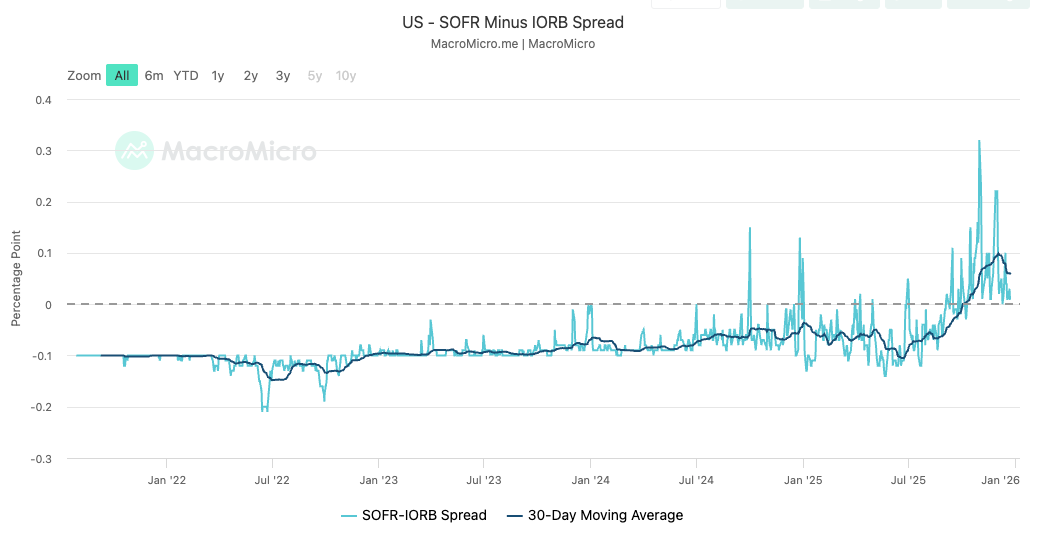

In fact, the Fed’s own framing is cautious: this is about maintaining rate control and preventing money-market weirdness from turning into policy slippage. The FT notes the program was framed as stabilizing money markets after QT-induced volatility, and the Fed recently ended QT this is the institutional memory of 2019 showing up again.

We can believe all of that and still trade the consequences.

Because “technical” actions still reprice the plumbing. And plumbing is where 2026 is likely to bite.

Overall there are a lot of potential upsides to this macro action. but with this there will be opportunities because some companies will still misuse the newfound liquidity to increase their risk doing things like doubling down tier three suppliers in China who may or may not be able to supply them depending on the whims of the CCP and what sector they are in. if its autos then no chance.

The tradeable part

We see five clean asymmetries, liquid, options-friendly, and mostly orthogonal to the daily outrage cycle.

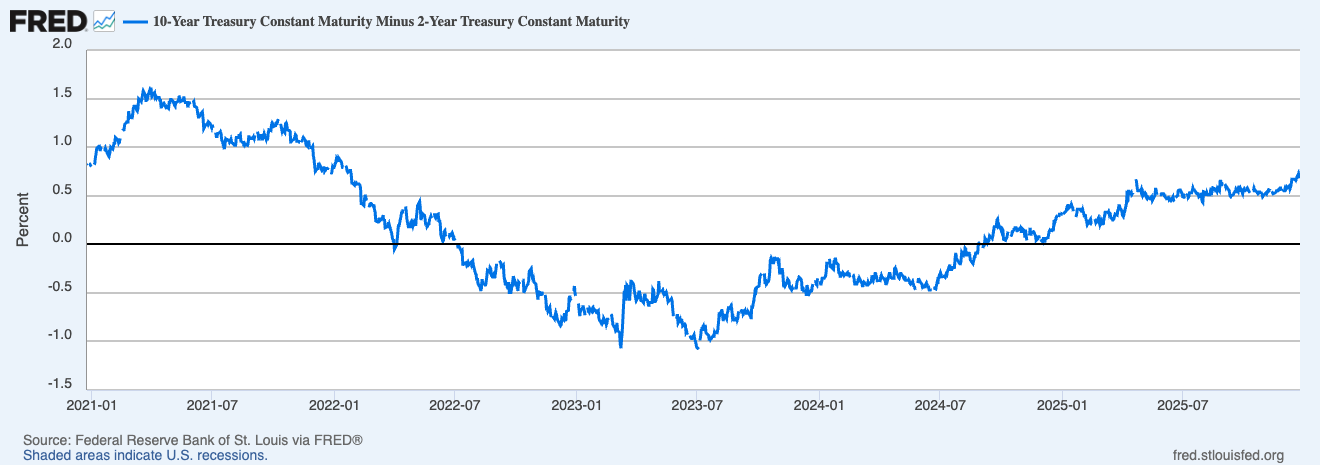

1) The curve steepener is still under-owned.

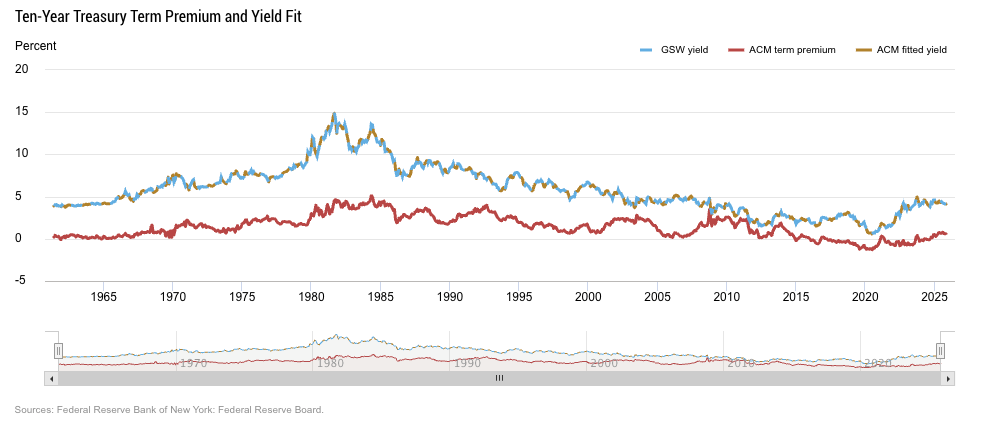

Rate cuts pull down the front end. Deficits and uncertainty keep the long end from following politely. Reuters has already pointed to steepening forces and rebuilding risk premia looking into 2026. Reuters

We don’t need a bond vigilante riot. We need the market to remember that term premium exists.

2) Own the tail where policy can’t jawbone it.

If 2026 gets even mildly messy—auction indigestion, inflation wobble, political noise—the long end reprices quickly. That’s not a “crash” call; it’s a convexity call. Own payer optionality. Don’t sell optionality to fund it.

3) Bills can richen even as issuance rises.

This is the most unintuitive one, which is exactly why it’s interesting. Treasury issues more bills. The Fed also buys bills. Net supply to private investors doesn’t have to rise the way the headline suggests—especially when the point is “ample reserves.” Federal Reserve Bank of New York

Front-end relative value trades get paid in basis points, and if you say “300 bips” in a meeting know that you are the worst person in there and should be shunned (jokes people)

4) Credit spreads are pricing “all boats,” but the regime screams “dispersion.”

Easier liquidity reopens windows. Windows are used. In a world where private markets have been waiting years for exits, “more liquidity” doesn’t just mean “everything rallies.” It also means inventory gets moved, and some of that inventory is not going to age well in daylight. Put bluntly all of the PE firms that have not been able to find exits for their investments over the last 5 years will see this new liquidity injection as a way to get out from things they dont want anymore, they will put lipstick on the pig.

We want quality carry, hedged with junk fragility: IG vs HY dispersion, sized like adults. No signal for panic in fact quite the opposite

5) The dollar can grind lower without becoming a religion.

There is no need to be “short USD” as a worldview. Seeing a move toward key support in DXY ~90/91 would be almost by design because with a lower dollar it will increase US exportability globally and we need to get back on top of that. Conveniently, the dollar is already down about 9.9% this year per Reuters, with further 2026 easing expectations weighing on it.

So we express it with put spreads: defined risk, defined objective, no martyrdom.

What would prove us wrong

The NY Fed’s bill purchases taper quickly and reserves stop rising (plumbing impulse fades). Federal Reserve Bank of New York

Treasury pivots back to duration meaningfully (bill share stalls; coupons ramp) at/after refunding. U.S. Department of the Treasury

Term premium falls despite fiscal supply and “risk premia” talk (duration bid overwhelms). Reuters

Credit markets widen broadly and persistently despite easier liquidity (refi window shuts; dispersion becomes correlation).

Closing

In 2026, the story won’t be “QE or not QE.” It’ll be simpler: are the pipes widening, and who gets to use them first?

Our bet is not doom. It’s mispricing: the market is underestimating how quickly a refi-and-exit regime changes outcomes—while overestimating how politely the long end will behave.

Ample reserves come with ample alibis. The curve doesn’t care.

Disclaimer: This is market commentary for informational purposes only, not investment advice.